OEO Blog: Rising Demand, Rising Stakes for the Electricity Grid

Over the past year, the OEO team have examining what the rapid growth of data centers and cryptocurrency mining means for the U.S. electricity system.

A warning sign came in December 2024, when capacity market clearing prices in PJM Interconnection jumped from $30 - $270 dollars per MW-day. That ninefold increase sent shock waves through the Mid Atlantic and Midwest and will ultimately show up in bills for roughly 67 million customers across 13 states. State leaders reacted strongly. But the price spike was not a random event. It was a market signal.

The suspected driver is the rapid growth in electricity demand from data centers and cryptocurrency mining operations. Recent estimates suggest that electricity use from these sources could increase 350 percent between 2020 and 2030, growing from about 4% of total U.S. electricity consumption to 9 percent. That is an extraordinary shift in a single decade for a sector that already operates at scale.

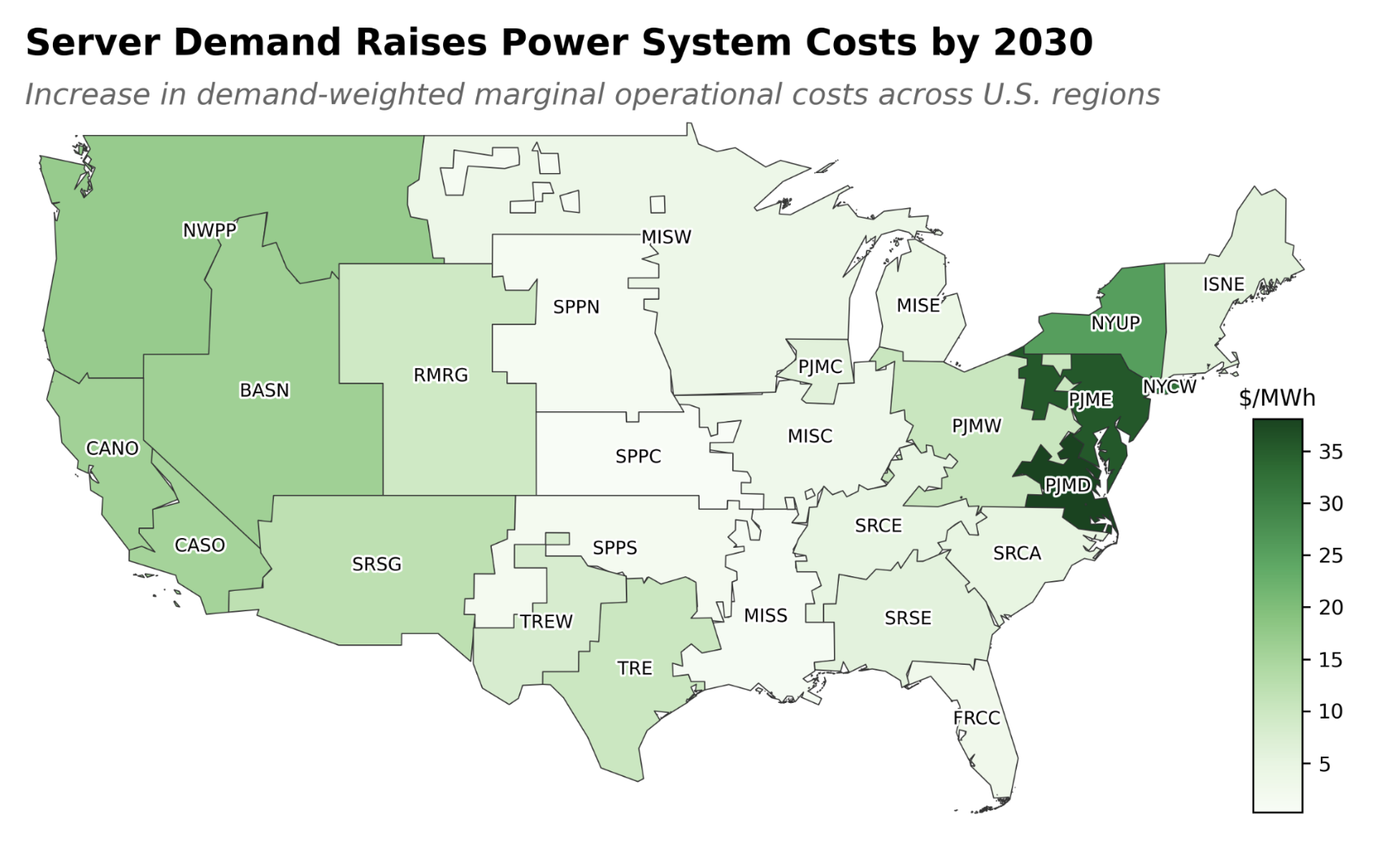

Through the Open Energy Outlook Initiative, my colleagues and I have modeled what this growth means under current policies and market structures, including the provisions of the Inflation Reduction Act that may be at risk. Our findings are clear. If we stay on our current path, wholesale electricity costs increase by an average of 8% nationally. In some regions the impacts are far larger. In Central and Northern Virginia, where the concentration of data centers is highest, we project cost increases exceeding 25% by 2030.

These cost increases are not abstract modeling artifacts. They reflect real grid planning challenges. In parts of the PJM region, more than 25 gigawatts of aging coal capacity that might otherwise retire are kept online to meet incremental demand from data centers. In the short run, running these plants can be less expensive than building new gas, renewable, or nuclear capacity. But that choice has consequences for both consumers and emissions.

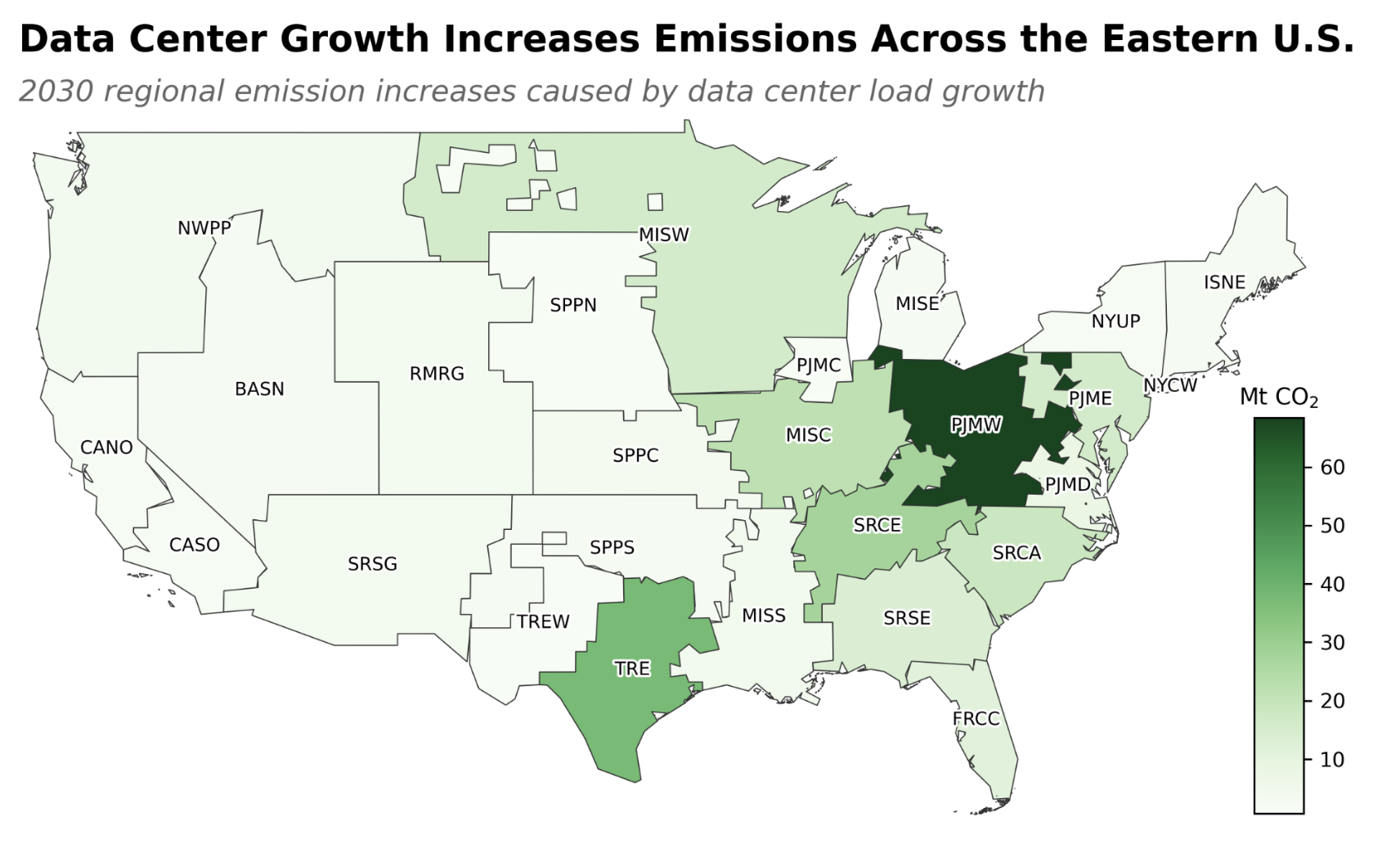

On the emissions side, the numbers are sobering. Under current policies, we estimate that additional data center and cryptocurrency mining load could increase power sector carbon dioxide emissions by 30 percent in 2030 relative to a case without that load growth. In absolute terms, that is about 275 million metric tonnes of carbon dioxide per year by 2030. To put that in perspective, that is roughly equivalent to the annual emissions of France.

The regional story also matters. In PJM, added demand is largely met by coal and natural gas, and some of the emissions are effectively shifted across state lines. This creates a form of carbon leakage where one state’s demand growth drives emissions in another state’s generators, complicating state level climate targets. By contrast, in Texas, targeted transmission investments and abundant wind resources make it more feasible to serve incremental load with lower emission generation. The same national trend can produce very different outcomes depending on regional resource availability and planning decisions.

What makes this moment particularly challenging is the speed of change. Traditional planning frameworks assume demand growth of one to two percent per year. In some localized areas, demand tied to data centers is growing at rates of 20% to 30% per year. Utility resource planning processes take years. Interconnection queues are already backlogged. Market mechanisms that are supposed to signal new investment are struggling to keep pace with sudden demand shocks.

The core issue is not whether data centers are good or bad. Digital infrastructure brings substantial benefits, including increased productivity from AI-based technologies. The question is how to integrate this growth into the power system without imposing disproportionate costs on consumers or undermining emissions goals.

There are policy tools available. Cost allocation and rate design reforms can ensure that large new loads contribute fairly to infrastructure investments. Strategic siting and stronger incentives for clean energy procurement can reduce pressure on carbon intensive generation. Transmission planning reform could unlock renewable rich regions and fundamentally alter projected cost and emission outcomes. Greater demand flexibility requirements, particularly for cryptocurrency mining and certain data center operations, may offer additional system benefits if implemented carefully.

None of these solutions is simple. They require coordination across federal, state, and regional authorities, as well as between public institutions and private firms. But the alternative is to let markets lurch from one price spike to the next while emissions climb.

When I look back at the December 2024 capacity auction in PJM, I see it as an early warning signal. The grid is telling us that something fundamental is changing. Our modeling suggests that higher costs and emissions are a likely outcome. But they are not inevitable. With thoughtful, proactive policy, we can accommodate digital economy growth while protecting affordability and continuing progress toward cleaner electricity.